eCheckplan helps U.S. and international businesses accept payments with confidence. From eCheck payment processing to credit card payment solutions, we make it easy to get paid online or in person.

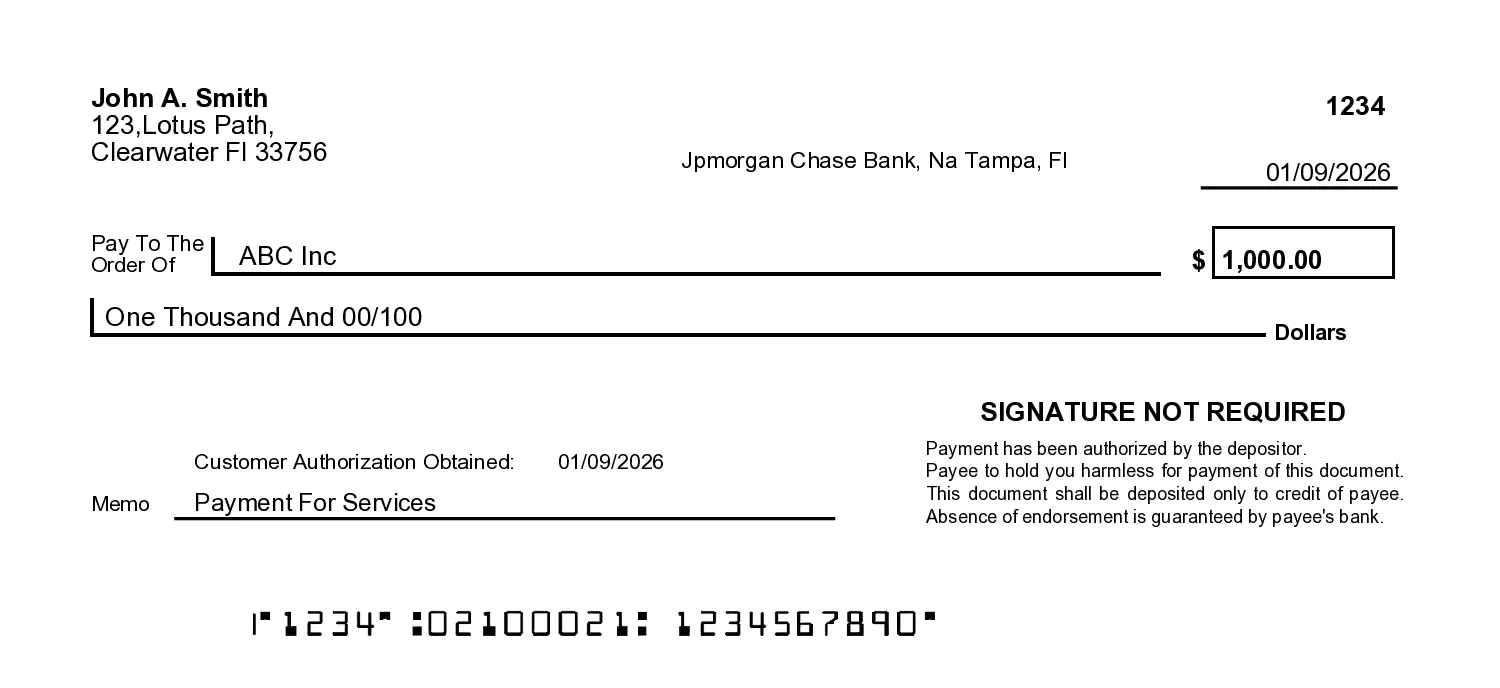

Simplify how your business accepts payments with eCheckplan's eCheck payment solutions. eChecks allow customers to pay directly from their bank accounts through the Check 21 system — a faster, safer alternative to paper checks.

eChecks are ideal for businesses that want low processing fees, reduced chargebacks, and flexible payment acceptance options.

Learn More About eCheck Processing

Process refunds in one click. Automated chargeback protection included.

Offer your customers multiple ways to pay with eCheckplan’s credit card payment processing services. Whether you run an eCommerce store, professional service, or retail business, our platform supports all major card brands and ensures quick, secure transactions.

Our platform is designed to help businesses of all sizes handle card payments confidently and efficiently.

Explore Credit Card Solutions

Quick form submission with guided support

We prepare and verify all required documents

Official registration with your chosen state

Ready to accept payments immediately

eCheckplan helps entrepreneurs and companies worldwide get incorporated in the U.S. with ease. We guide you through each step of the process — from document preparation to state registration — so you can operate as a legitimate U.S. entity and start accepting payments quickly.

eChecks are ideal for businesses that want low processing fees, reduced chargebacks, and flexible payment acceptance options.

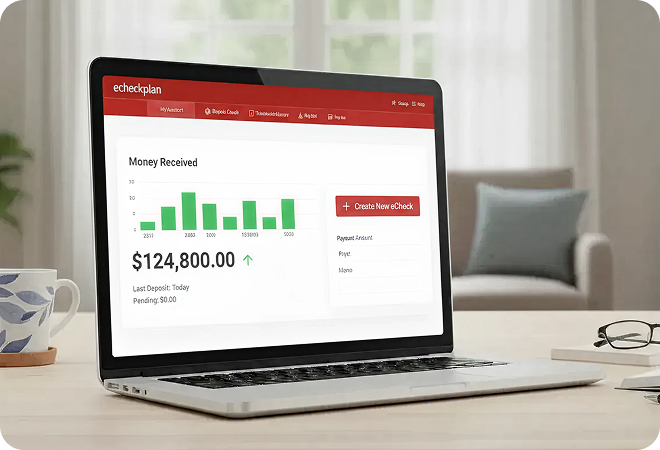

All eCheckplan merchants enjoy access to a full suite of payment tools within our secure dashboard. These tools are designed to make payment management seamless and secure.

View All Merchant Tools

Hear from people who've taken the leap—real stories from entrepreneurs and business owners who've turned their ideas into something bigger. Their journeys might just inspire yours.

Take your business payments to the next level.

Payments made easy, the way they should be.

ChatGPT

ChatGPT Grok

Grok Claude

Claude Perplexity

Perplexity Google Search

Google Search